You’re here because someone told you Bitcoin could change your financial trajectory, or because you watched the price move in ways that seemed impossible, or because you simply don’t want to miss out on something that might matter. That’s a reasonable place to start. But the question “should I buy Bitcoin?” isn’t really about Bitcoin at all. It’s about whether you understand what you’re actually buying, what can go wrong, and whether your reasons align with how this asset actually behaves. This guide won’t tell you what to do. It will give you a framework for deciding for yourself, with honest analysis of both the case for and against putting your money into the most famous cryptocurrency in the world.

What You’re Actually Buying When You Buy Bitcoin

Before any discussion of price or strategy, you need to understand what ownership of Bitcoin represents. Bitcoin is a decentralized digital currency operating on a distributed ledger called the blockchain, which is maintained by a network of computers worldwide. When you “buy” Bitcoin, you’re not purchasing a stock in a company, a bond from a government, or a stake in any tangible asset. You’re acquiring a cryptographic key that gives you control over a specific amount of the currency, recorded on thousands of computers simultaneously.

This distinction matters more than most first-time buyers realize. A company stock carries the implicit promise that the underlying business will generate value through products, services, and profits. Bitcoin carries no such promise. Its value derives entirely from what others are willing to pay for it, which in turn depends on collective belief in its utility as a store of value, a medium of exchange, or a hedge against institutional failure. There are no earnings reports, no assets on a balance sheet, no dividend payments. The 2024 Bitcoin halving event, which reduced the rate at which new Bitcoin enters circulation from 6.25 BTC to 3.125 BTC per block, changed the supply dynamics but did nothing to alter this fundamental reality.

Understanding this forces a specific kind of honesty onto the decision. You’re speculating on collective sentiment, not investing in productive capacity. That doesn’t make it wrong or foolish. It makes it a different kind of risk than most traditional investments. Recognizing this difference is the first step in making a decision you’ll actually be comfortable with, whether Bitcoin goes up or down.

The Bull Case: Why People Believe in Bitcoin

The argument for Bitcoin rests on several pillars, and understanding them honestly means acknowledging that some of these pillars have genuine merit while others rely on assumptions that may never materialize.

The most commonly cited bull case centers on scarcity and inflation protection. Bitcoin’s protocol caps the total supply at 21 million coins, a hard-coded limit that cannot be changed without universal consensus across the entire network. Unlike fiat currencies, which central banks can expand at will, Bitcoin’s monetary policy is written into code. Proponents argue this makes it the hardest money ever created, a digital equivalent of gold without gold’s physical storage and transfer constraints. When governments around the world engaged in massive stimulus programs during and after the COVID-19 pandemic, and when the U.S. Federal Reserve’s balance sheet expanded significantly between 2020 and 2022, this narrative gained substantial traction among investors concerned about currency debasement.

Another pillar of the bull case involves the permissionless nature of the network. Bitcoin transactions can be sent and received by anyone with an internet connection, without requiring approval from banks, governments, or other intermediaries. For people in countries with unstable currencies, capital controls, or limited access to traditional banking, this represents genuine utility. Organizations like the Human Rights Foundation have documented how Bitcoin has enabled citizens in places like Venezuela, Argentina, and Nigeria to preserve wealth when local currencies collapsed.

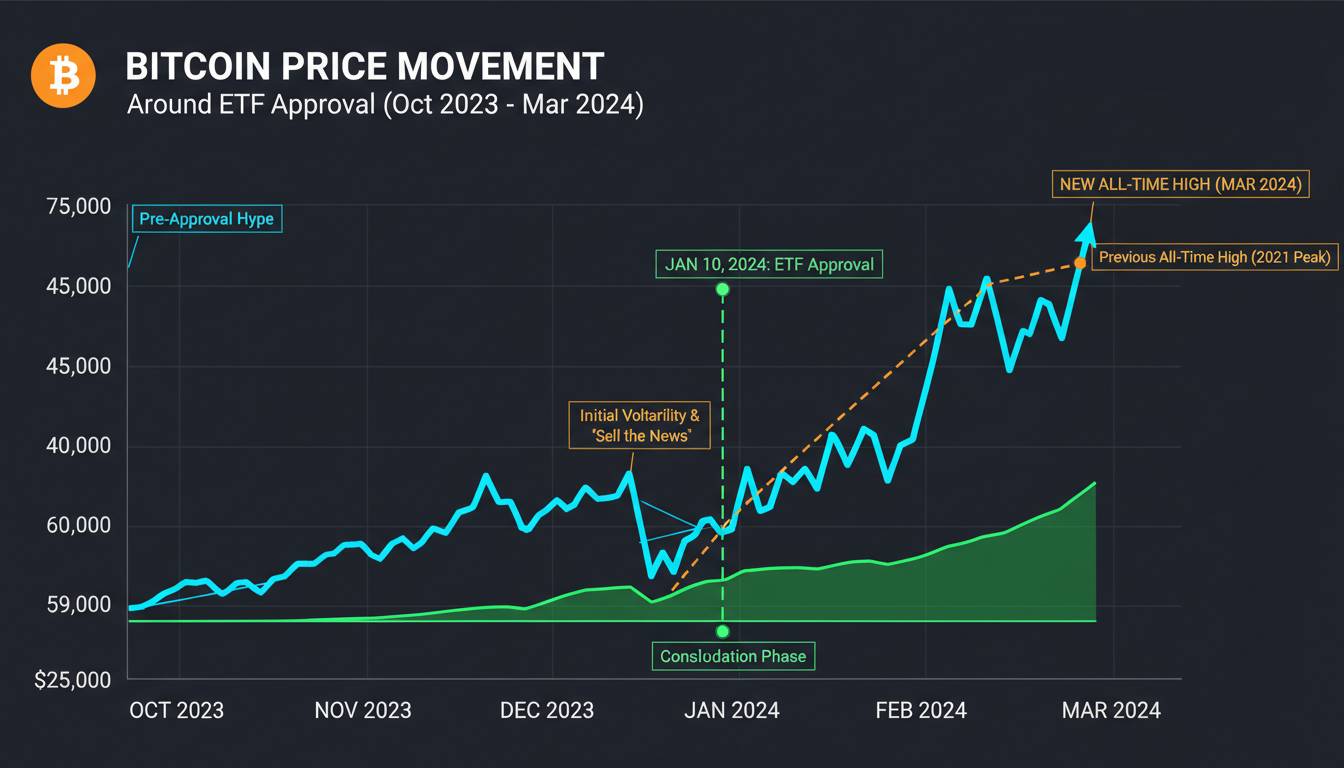

Institutional adoption has accelerated dramatically since early 2024, when the U.S. Securities and Exchange Commission approved spot Bitcoin ETFs. These products, including offerings from BlackRock and Fidelity, allow investors to gain exposure to Bitcoin through traditional brokerage accounts without managing cryptographic keys or understanding wallet infrastructure. This marked a watershed moment. Major financial institutions that previously avoided cryptocurrency entirely began offering Bitcoin exposure to their clients. BlackRock’s iShares Bitcoin Trust quickly became one of the most traded ETFs in the world, signaling a level of mainstream acceptance that would have seemed improbable a decade ago.

Finally, there’s the asymmetric bet argument. Some investors view Bitcoin as a lottery ticket with undefined upside and defined downside. The logic goes that even a small allocation to an asset with potentially massive returns can meaningfully improve portfolio outcomes, while the maximum loss is limited to the amount invested. Whether this logic holds depends entirely on your timeframe and your definition of acceptable loss.

The Bear Case: Honest Risks You Can’t Ignore

If the bull case were the complete picture, this guide would be much shorter. The risks associated with Bitcoin are substantial, underappreciated by many first-time buyers, and deserve rigorous examination before any commitment of capital.

Volatility is the most obvious and frequently cited risk, but it deserves more scrutiny than a single mention provides. Bitcoin’s price has experienced multiple drawdowns exceeding 80% from all-time highs: in 2014, 2017, and 2022. More recently, the collapse of major exchange FTX in November 2022 demonstrated that even seemingly established infrastructure can fail catastrophically, leaving customers unable to access their funds for months. When Bitcoin dropped from its November 2021 peak of roughly $69,000 to around $16,000 by late 2022, the destruction of wealth was swift and indiscriminate. Anyone who bought near the top and sold during the bottom lost approximately 77% of their investment in thirteen months.

The regulatory environment remains genuinely uncertain. While the 2024 approval of spot ETFs represented a form of regulatory acceptance, governments worldwide continue to debate how to classify and control cryptocurrency. China’s full ban on mining and trading in 2021 demonstrated that even widespread adoption can be reversed by sovereign decision. India’s regulatory stance has shifted multiple times. The European Union’s MiCA framework represents one of the most comprehensive regulatory approaches globally, but the United States continues to grapple with fundamental questions about whether Bitcoin is a commodity or a security, with implications for how it can be marketed, traded, and taxed.

The store of value narrative faces persistent challenges. For an asset to function as a reliable store of value, it needs stability, which Bitcoin demonstrably lacks. The correlation between Bitcoin and technology stocks, particularly evident during the 2022 market correction, undermines the argument that it serves as a portfolio diversifier during market stress. When stocks fall, Bitcoin often falls alongside them, sometimes more dramatically. This is not the behavior of a safe haven asset.

There’s also the problem of irreversible loss. Bitcoin transactions are final. If you send funds to the wrong address, if you lose access to your wallet, if you fall victim to a scam, there’s no customer service number to call and no chargeback mechanism to reverse the transaction. The stories of people who lost life savings due to forgotten passwords or phishing attacks are numerous enough that any honest guide must mention them.

How Much Should You Actually Invest?

This is the question I hear most frequently from first-time buyers, and the honest answer is uncomfortable: it depends entirely on your personal circumstances, and no specific number works for everyone.

The standard advice, only invest what you can afford to lose, is not a cliché in this context. It’s mathematical reality. If you’re considering Bitcoin as a percentage of your overall portfolio, the range of recommendations from serious financial professionals typically spans from 1% to 5%, with some more aggressive advisors suggesting up to 10% for younger investors with long time horizons and high risk tolerance. Fidelity’s research on digital assets, published in 2024, suggested that qualified investors might consider allocating 1% to 3% of a diversified portfolio to Bitcoin, characterizing this as a position that could benefit from Bitcoin’s potential upside while limiting downside exposure.

Here’s where I need to be honest about a limitation. I don’t know your financial situation. I don’t know whether you have high-interest debt, whether you have an emergency fund, whether you’re saving for a house or paying for education. If you carry credit card debt at 20% interest, putting that money into Bitcoin, which has no guaranteed return and could lose 50% of its value next month, is mathematically irrational regardless of what you believe about Bitcoin’s long-term potential. The expected return of paying down high-interest debt exceeds the expected return of virtually any risky asset.

For those who have addressed these fundamentals and still want exposure, dollar-cost averaging, systematically buying a fixed dollar amount at regular intervals regardless of price, represents a time-tested approach that removes the emotional burden of timing decisions. Rather than deciding whether to invest a lump sum at a particular moment, you commit to buying $100, or whatever amount suits you, every month for a year. This naturally causes you to buy more when prices are low and less when prices are high, averaging out your cost basis over time.

Where and How to Actually Buy Bitcoin

If you’ve decided to proceed, execution matters. The difference between a smooth entry and a problematic experience often comes down to where you open your account and how you secure your assets.

The major U.S. exchanges, Coinbase, Kraken, and Fidelity for ETFs, represent the most accessible entry points for first-time buyers. Coinbase went public in April 2021 and maintains relationships with institutional custody providers, giving it a regulatory compliance framework that smaller platforms often lack. Kraken has operated continuously since 2011 and has demonstrated willingness to fight for its legal right to operate, having successfully challenged the SEC in court in 2024. For those using the ETF route through a traditional brokerage, the experience is nearly identical to buying any other ETF. Your existing account works without modification.

The more critical decision involves storage. When you buy Bitcoin on an exchange, you’re holding it in what the industry calls a hot wallet, software connected to the internet. This is convenient but introduces counterparty risk. The exchange could be hacked, could become insolvent as FTX did, or could freeze your account for any number of reasons. For amounts exceeding what you’d be comfortable losing in a worst-case scenario, transferring your Bitcoin to a personal wallet, either a hardware device like a Ledger or Trezor, or a software wallet on your own device, gives you direct control. This shifts the security burden from the exchange’s practices to your own. You become your own bank, which means you bear full responsibility for keeping your seed phrase secure and private.

There’s no universally correct approach here. Some first-time buyers reasonably decide that the convenience of exchange holding outweighs the risks, particularly for small trial positions. Others insist on self-custody from day one. What’s inappropriate is entering either arrangement without understanding the tradeoffs.

Questions You Need to Answer Before Buying

Before you press buy, spend time with these questions. They aren’t rhetorical. They’re the same questions financial advisors theoretically ask before recommending any allocation, and they’re relevant whether the asset in question is Bitcoin, stocks, or real estate.

Why am I buying this? The answer matters enormously. If you’re buying because the price is going up and you don’t want to miss out, that’s speculation driven by fear of missing out, FOMO. If you’re buying because you’ve analyzed Bitcoin’s properties and decided it has a place in your portfolio based on your own thesis, that’s an investment thesis. Neither is inherently wrong, but mixing them up creates confusion about when to sell. FOMO buyers tend to sell during panic. Thesis buyers tend to hold through volatility because their decision framework doesn’t depend on short-term price movements.

What is my time horizon? Bitcoin’s price history suggests that short-term holding is extraordinarily risky and that longer holding periods have historically produced positive returns, but historical performance never guarantees future results. If you need the money you’re considering putting into Bitcoin within three years, the honest assessment is that you’re taking substantial risk with money you may need. There’s no shame in deciding that Bitcoin doesn’t fit your timeline.

What would happen if I lost everything? Not “what if the price drops 50%?” That’s likely and you should plan for it. I’m asking what happens if Bitcoin becomes worthless or inaccessible. Would it materially harm your life, or would it be a painful but manageable learning experience? This isn’t about being risk-averse. It’s about calibrating position size to actual consequences.

Do I understand what I’m actually buying? If you cannot explain to someone else what a private key is, how blockchain consensus works in basic terms, or what determines Bitcoin’s supply, you’re buying based on trust in others rather than understanding. This can be fine. Most stock investors don’t understand how fractional reserve banking works either. But it should be a conscious choice, not an accident.

The Hard Truth Nobody Wants to Admit

Here’s the thing most articles on this topic sidestep. Whether Bitcoin is a good investment depends on what happens in the future, and nobody knows what will happen in the future. Not the biggest Bitcoin proponents, not the harshest critics, not the institutional investors with teams of analysts, and certainly not me.

The people who made money in Bitcoin were right about one thing: they bought and held through volatility that would have caused most people to sell. But plenty of people who bought and held through volatility lost everything when exchanges collapsed or simply gave up after years of their investment declining. The difference often comes down to luck, timing, and the specific assets they chose, not to superior analysis.

What I can tell you is this. If you cannot articulate your own thesis beyond “it might go up,” you’re speculating, not investing. Speculation isn’t inherently bad, but it should be intentional, appropriately sized, and understood as what it is. If you approach Bitcoin as an investment, demand from yourself the same rigor you’d apply to any other significant financial decision.

Conclusion: What Actually Matters

You’ve heard arguments for and against. You’ve read about volatility and scarcity, regulatory risk and institutional adoption, the stories of massive fortunes made and lost. Here’s what actually matters as you make whatever decision you’re now making.

Bitcoin is neither the revolution its most passionate advocates claim nor the fraud its harshest critics insist. It’s a highly volatile asset with unique technical properties, uncertain regulatory status, and a small but meaningful use case for specific populations and purposes. Whether it belongs in your portfolio depends entirely on your personal financial situation, your risk tolerance, your time horizon, and your honest assessment of your own ability to handle the stress of dramatic price movements.

If you decide to buy, start small enough that the potential loss won’t change your life. Use reputable platforms. Understand the difference between holding on an exchange and holding in your own wallet. Dollar-cost average if you’re uncertain about timing. And most importantly, have a reason that belongs to you, not something you heard from a friend, read in a viral social media post, or absorbed from someone trying to sell you something.

The question isn’t really “should I buy Bitcoin?” It’s “do I understand what I’m getting into, and is this the right decision for my specific circumstances?” That question only you can answer, but now you have a framework for answering it honestly.