When the S&P 500 plunges, cryptocurrency doesn’t just dip—it often freefalls. This isn’t coincidence, and understanding why matters for anyone holding digital assets. The correlation between traditional markets and crypto has strengthened dramatically since 2020, turning what was once an independent asset class into something that frequently moves in lockstep with stocks. The implications are significant: crypto no longer serves as the portfolio hedge many investors assumed it would be. Here’s what’s actually driving this relationship—and what smart investors do differently.

Institutional Investors Created the Link

The single most important factor linking crypto to the stock market is simple: institutions now own both.

Before 2020, cryptocurrency was predominantly a retail phenomenon. Bitcoin was something you bought on curiosity or ideology; it had minimal presence in pension funds, hedge portfolios, or corporate treasuries. That changed. BlackRock launched its Bitcoin trust in 2021. Fidelity offered 401(k) crypto options. Major banks like Morgan Stanley and Goldman Sachs began offering crypto exposure to wealthy clients. By 2023, CoinShares estimated that institutional investors held over $60 billion in crypto assets globally.

This created a structural connection that didn’t exist before. When institutional portfolio managers face margin calls or need to raise cash quickly, they don’t check whether an asset is “digital” or “traditional”—they check the liquidity and mark-to-market losses. A hedge fund with both tech stocks and Bitcoin on its books will sell whichever position is easiest to exit when liquidity dries up. The result: correlated selling pressure.

Ray Dalio, founder of Bridgewater Associates, noted in a 2022 interview that the traditional portfolio construction assumption—that uncorrelated assets protect against market downturns—has become much harder to achieve as previously independent assets like crypto now behave similarly during stress. This matters because it means the diversification argument for crypto has fundamentally shifted.

Risk-Off Sentiment: When Markets Panic, Everything Falls

Human psychology doesn’t distinguish between asset classes when fear takes hold. The “risk-off” phenomenon describes a specific market condition where investors flee anything perceived as risky—stocks, corporate bonds, real estate, and yes, cryptocurrency—while fleeing toward perceived safety: government bonds, the US dollar, and cash.

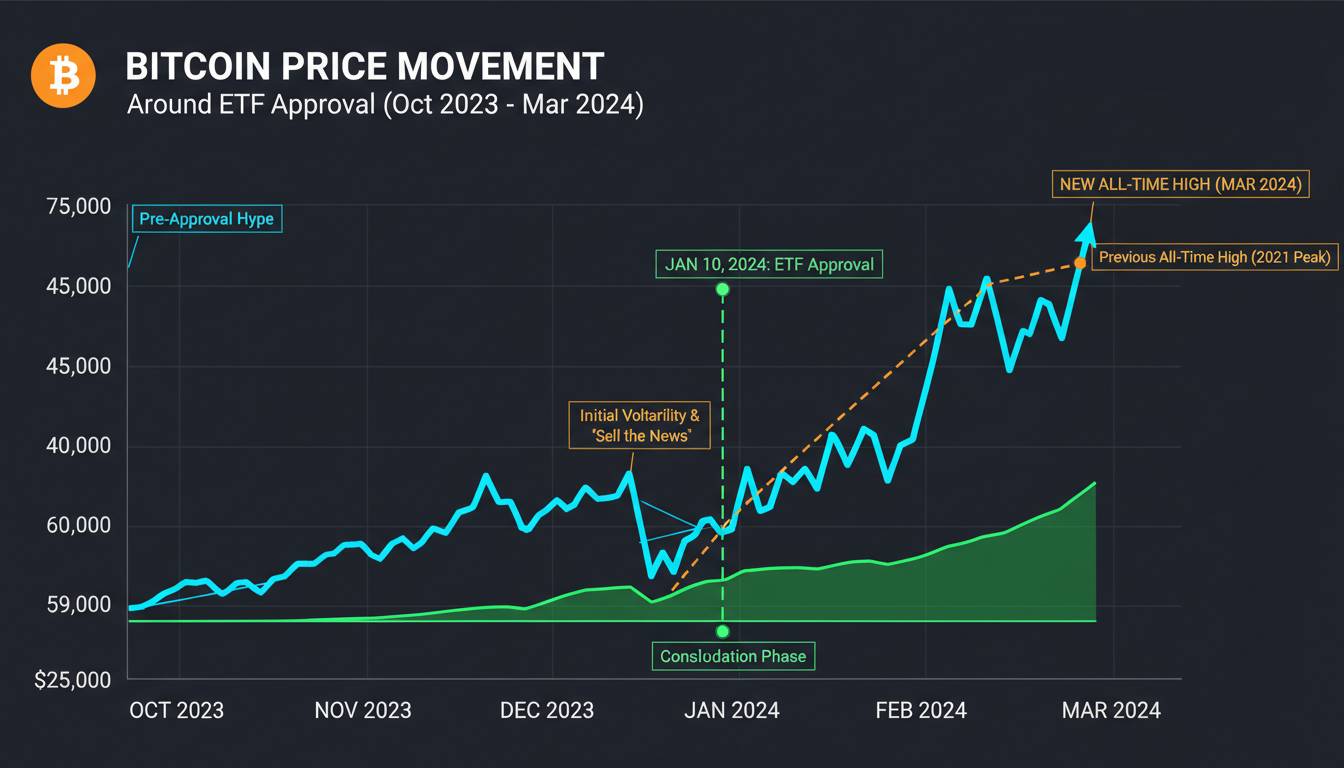

This sentiment shift happens faster than most people realize. In March 2020, when COVID-19 fears peaked, the VIX (volatility index measuring stock market fear) spiked to 82—the highest level since the 2008 financial crisis. Within days, Bitcoin fell over 50% from its yearly high. It wasn’t because COVID-19 specifically affected blockchain technology. It was because traders globally moved into risk-off mode.

The mechanism works like this: when macroeconomic uncertainty rises, algorithmic trading systems automatically reduce exposure to “risk assets.” Many quant funds and exchange-traded products use correlated volatility signals that trigger sells across multiple asset classes simultaneously. Crypto, despite its early history as a countercultural alternative to mainstream finance, now trades on the same exchanges, through the same brokerage platforms, and is accessed by the same traders using similar technical analysis tools. The result is synchronized selling.

What surprises many investors is how quickly this can reverse. During the 2020 recovery, Bitcoin actually outpaced stocks dramatically, rising over 160% from March lows while the S&P 500 recovered roughly 50% in the same timeframe. Risk-on sentiment can benefit crypto just as dramatically—but you can’t predict which direction the sentiment truck is heading.

Liquidity Disappears When You Need It Most

Here’s an uncomfortable truth about crypto that became painfully obvious in 2022: the market that looks most liquid during bull runs becomes remarkably illiquid during crashes.

When stock markets decline significantly, liquidity across all markets tends to constrict. This is particularly damaging for crypto because the asset class is heavily dependent on continuous buyer interest to maintain prices. Unlike stocks, where companies can repurchase shares or pay dividends to support value, cryptocurrency has no such mechanisms. Price is purely a function of supply and demand.

During the 2022 crypto winter, major lending platforms like Celsius and Three Arrows Capital collapsed precisely because they couldn’t meet withdrawal demands. These weren’t small players—they had billions in combined assets. The cascading failures revealed a fundamental vulnerability: crypto liquidity is largely contingent on confidence. When confidence erodes, the “flight to liquidity” means investors sell what they can, when they can, at whatever price is available.

This is why you see such dramatic price dislocations during major selloffs. In November 2022, when FTX imploded, Bitcoin dropped below $16,000—a 75% decline from its all-time high. The stock market, while declining, didn’t experience equivalent percentage drops. The lesson: crypto’s liquidity advantage disappears exactly when you need it most.

Interest Rates and Macroeconomic Factors Affect Both Markets

The Federal Reserve’s policy decisions now ripple through cryptocurrency with surprising force. When interest rates rise, two things happen that hurt crypto: risk-free returns become more attractive (making yield-bearing assets more competitive), and borrowing costs increase (reducing the leverage that fuels many crypto trading strategies).

This connection became undeniable in 2022. The Federal Reserve raised rates seven times throughout the year, pushing the benchmark rate from near-zero to over 4%. Bitcoin fell roughly 65% in 2022. The S&P 500 dropped about 19%. Both declined—and they declined together—because both were responding to the same macroeconomic reality: cheap money was ending.

Cryptocurrency, particularly Bitcoin, has increasingly behaved like a “tech stock on steroids.” When interest rates were near zero, capital was cheap, and investors loaded up on speculative assets. As rates rose, that dynamic reversed. The cryptocurrency market’s sensitivity to rate expectations means it now functions almost like a high-beta version of tech stocks—moving in the same direction but with amplified magnitude.

This isn’t a temporary fluctuation. If central banks globally continue fighting inflation through monetary tightening, or if new rate-cutting cycles begin, these macroeconomic factors will continue driving correlation. The days of crypto ignoring Federal Reserve announcements are over.

Historical Examples: When the Correlation Became Obvious

The 2022 market collapse remains the clearest demonstration of crypto-stock correlation. Between November 2021 and November 2022, Bitcoin lost roughly 75% of its value while the Nasdaq (heavily weighted toward tech stocks) dropped approximately 33%. Both peaked in November 2021 and both hit their lows in late 2022, roughly simultaneously.

More concerning for crypto proponents: the correlation didn’t exist only during the crash. Bloomberg data from early 2023 calculated the 90-day correlation between Bitcoin and the S&P 500 at 0.71—a strongly positive correlation indicating they moved in the same direction most of the time. Prior to 2020, that correlation was often near zero or slightly negative.

The March 2020 COVID crash provided an earlier preview. When markets panicked in mid-March, Bitcoin dropped from roughly $9,000 to under $5,000 in 48 hours—a steeper percentage decline than the S&P 500 experienced. The recovery was equally dramatic: Bitcoin reached new all-time highs by December 2020, while stocks took longer to recover their previous highs.

2024 has shown mixed signals. Early 2024 saw some decoupling, with Bitcoin performing strongly even as stocks wobbled amid rate cut uncertainty. However, the relationship remains close enough that major stock market declines typically produce crypto declines as well. The correlation may weaken over time—but it hasn’t broken.

Will Crypto Decouple From Stocks?

This is the question on every crypto investor’s mind, and the honest answer is probably not entirely, and not soon.

Several structural factors ensure continued correlation. First, institutional involvement won’t reverse—major financial institutions have too much infrastructure invested in crypto to exit. Second, regulatory frameworks increasingly treat crypto as a mainstream financial asset, which brings it further into the traditional market ecosystem. Third, the macroeconomic factors driving both markets (interest rates, inflation, global liquidity) aren’t going away.

However, some decoupling factors could emerge. If a major government or corporation adopts Bitcoin as a treasury reserve asset—as some US states have recently considered and companies like MicroStrategy have already done—it could create demand drivers unrelated to stock market performance. Similarly, real-world asset tokenization (real estate, commodities, stocks on blockchain) could eventually create utility demand that supports crypto independently of speculative trading.

But these are future possibilities, not current certainties. For now, treating crypto as a correlated risk asset—rather than an uncorrelated diversifier—is the prudent approach.

Frequently Asked Questions

Is crypto correlated to the stock market?

Yes, the correlation between cryptocurrency and stock markets has strengthened significantly since 2020. Bloomberg and CoinMetrics research documents 60-70% correlation during bear markets. While correlation isn’t perfect, it’s strong enough that crypto no longer provides meaningful diversification during stock market declines.

Why does crypto follow the stock market?

Three primary factors drive this: institutional investors holding both asset classes, risk-off sentiment causing simultaneous selling across all risky assets, and macroeconomic factors (particularly interest rates) affecting both markets similarly. When institutional portfolio managers need to reduce risk, they sell crypto alongside stocks.

Does crypto crash before the stock market?

Not consistently. During the 2022 bear market, both peaked in November 2021 and hit bottom simultaneously in late 2022. However, crypto’s higher volatility means percentage drops are typically larger and faster. Crypto can crash independently (as with FTX in 2022), but it more commonly falls alongside stock markets rather than leading them.

Will crypto recover when the stock market recovers?

Historically, yes—when risk-on sentiment returns, crypto has often recovered faster and more dramatically than stocks. However, past performance doesn’t guarantee future results. The strength of any recovery depends on whether new money enters the market and whether macro conditions (interest rates, liquidity) become favorable again.

What Smart Investors Do Differently

Understanding this correlation should change how you approach crypto allocation. Rather than treating it as an uncorrelated alternative, consider these practical adjustments.

First, reduce allocation size. If crypto behaves like a risk asset, it should occupy the same portfolio slot as other high-risk assets—meaning a smaller percentage than many currently hold. Second, time horizon matters more than ever. Crypto’s volatility means you need either extraordinary patience (holding through multi-year cycles) or rigorous discipline (strict exit strategies during mania phases). Third, don’t rely on crypto as emergency liquidity. Given liquidity contraction during crises, assume you may not be able to exit at anything close to stated value during market stress.

The crypto market isn’t going away. It’s become a legitimate, albeit volatile, asset class with institutional infrastructure and growing mainstream adoption. But the old narrative that crypto moves independently from traditional markets is dead. Understanding this correlation isn’t about pessimism; it’s about building portfolios that acknowledge reality rather than hoping for idealized assumptions.