The relationship between the Securities and Exchange Commission and cryptocurrency markets resembles a long-running negotiation where one party keeps changing the terms. What began as cautious curiosity in 2014 has evolved into an enforcement-first approach that has simultaneously suppressed certain market activities while inadvertently driving innovation elsewhere. Understanding this decade-long arc isn’t just historical interest—it explains why the crypto industry looks the way it does today, why certain projects thrived while others collapsed, and where things might go from here.

This timeline traces the SEC’s involvement with digital assets from early guidance through the spot Bitcoin ETF approval in January 2024, examining the enforcement actions that reshaped the industry and the market responses that followed.

The SEC’s first formal statements about cryptocurrency arrived not through enforcement but through investor alerts and staff statements. In 2014, the SEC’s Investor Alert section published guidance warning about the risks of Bitcoin and virtual currencies, marking the agency’s initial recognition that digital assets had reached sufficient market prominence to warrant attention.

This early period was characterized by regulatory ambiguity rather than aggression. The SEC acknowledged Bitcoin’s existence while declining to classify it as a security—a distinction that would become central to subsequent enforcement battles. The distinction matters enormously: securities fall under SEC jurisdiction and require extensive registration or exemption, while commodities like gold fall under the Commodity Futures Trading Commission’s purview.

The real inflection point arrived in July 2017 with the publication of the DAO Report. The DAO (Decentralized Autonomous Organization) was a venture capital fund built on Ethereum that had raised $150 million in Ether through a token sale. The SEC analyzed the transaction and concluded that the DAO tokens constituted investment contracts—and therefore securities—under the Howey test, a framework from 1946 determining whether a transaction qualifies as an investment contract.

The DAO Report didn’t announce new regulations. It announced a new interpretive framework that would guide enforcement for the next seven years. The SEC’s reasoning was straightforward: despite the blockchain technology underlying the transaction, investors were motivated by expectations of profit derived from the efforts of others—the DAO’s founders and developers. This interpretation became the foundation for treating most token sales as securities offerings, regardless of how decentralized the project claimed to be.

2017-2020: The ICO Crackdown

Following the DAO Report, the SEC shifted from guidance to enforcement with remarkable speed. Between 2017 and 2018, the agency launched dozens of enforcement actions related to Initial Coin Offerings, treating virtually every token sale as a potential securities violation unless the issuer could demonstrate clear exemptions.

The enforcement strategy during this period was primarily punitive rather than preventive. The SEC pursued cases against both major projects and small-time scammers, establishing precedent through settlements and court judgments. Among the notable cases from this era, the SEC’s 2019 action against Telegram stood out. The messaging app company had raised $1.7 billion through Gram token sales, and the SEC obtained a preliminary injunction blocking the token distribution. Telegram ultimately agreed to return $1.2 billion to investors and pay $18.5 million in penalties—a settlement that demonstrated the agency’s willingness to pursue high-profile targets regardless of their prominence.

During this same period, the SEC created the Cyber Unit in 2017, specifically tasking a team within the Enforcement Division with pursuing securities law violations involving distributed ledger technology. The unit’s formation signaled institutional prioritization of crypto enforcement, transforming what had been scattered actions into a coordinated strategy.

The practical impact on markets was immediate. Many legitimate blockchain projects relocated outside the United States or abandoned token sales entirely. The United States gained a reputation as a hostile regulatory environment—a characterization that industry advocates would spend years attempting to reverse. Initial coin offerings, which had dominated 2017’s crypto market, declined precipitously in the subsequent years.

Yet enforcement during this era also served a legitimate investor protection function. The crypto space in 2017-2018 was plagued by outright fraud: Ponzi schemes disguised as blockchain projects, teams that raised funds and immediately abandoned their roadmaps, and marketplaces filled with tokens that had no real utility. The SEC’s enforcement actions, while aggressive, corresponded with a decline in obvious fraud within U.S.-focused projects.

2019-2021: The Hinman Era and Enforcement Maturation

In June 2019, SEC Director of Corporation Finance William Hinman delivered a speech that would become one of the most consequential documents in crypto regulatory history. The “Hinman Speech” attempted to provide clarity on when a digital asset might no longer be considered a security.

The framework Hinman proposed was elegant in theory: when a digital asset is sufficiently decentralized such that purchasers no longer reasonably expect profits from the efforts of a particular team or group, it may no longer qualify as a security. Bitcoin and Ethereum, Hinman suggested, had likely reached that threshold—though he was careful to note this was his own view and not formal agency policy.

The practical application proved far messier than the theory. No clear criteria existed for what “sufficiently decentralized” meant, and projects attempting to rely on the Hinman framework had no reliable method of determining whether they had crossed the threshold. The speech provided rhetorical cover for the industry while offering no enforceable safe harbor.

The Ripple case, filed in December 2020, tested the SEC’s enforcement theory against a major project that explicitly rejected the agency’s characterization. The SEC alleged that Ripple, the company behind the XRP token, had conducted an unregistered securities offering worth $1.38 billion. Ripple’s defense centered on the Hinman Speech’s logic: XRP was sufficiently decentralized that Ripple the company was not the essential driver of token value.

The case dragged on for years, creating prolonged uncertainty. Both sides claimed victory at various points—Ripple achieved favorable rulings on certain procedural matters while the SEC maintained its core theory. The case’s ultimate resolution remains uncertain, but it has consumed enormous resources from both parties and demonstrated the limitations of enforcement-first regulatory approaches.

2021-2023: The Gensler Aggression

When Gary Gensler became SEC Chair in April 2021, the agency’s posture toward crypto shifted dramatically. Gensler, a former Goldman Sachs partner who had taught courses on blockchain at MIT, brought deep technical knowledge and an aggressive enforcement philosophy. His public statements repeatedly characterized the crypto markets as “rife with fraud and abuse” and asserted that the vast majority of digital assets qualified as securities.

The Gensler era produced an unprecedented wave of enforcement actions. In 2022 alone, the SEC filed over 100 crypto-related enforcement actions—a record by a substantial margin. The cases targeted not only token issuers but also exchanges, lending platforms, and DeFi protocols.

The most consequential cases from this period involved major U.S. exchanges. In February 2023, the SEC charged Coinbase with operating as an unregistered securities exchange, broker, and clearing agency. The charging document named 20 tokens that the SEC alleged were securities traded on Coinbase’s platform—a list that included established assets like Solana and Polygon, raising questions about whether the agency’s theory could potentially apply to most cryptocurrencies traded on major exchanges.

The Binance case, filed simultaneously in February 2023, targeted the world’s largest crypto exchange. The SEC alleged that Binance had operated unregistered exchanges, offered unregistered securities, and manipulated markets through a trading firm affiliated with the exchange. The case was particularly significant because Binance’s global market share dwarfed other exchanges, and the SEC’s action sent shockwaves through global crypto markets.

The market impact of this enforcement period was severe but complicated. The crypto market capitalization collapsed from approximately $3 trillion in late 2021 to around $800 billion by late 2022—a decline driven primarily by the broader economic environment and specific company failures (Terra/Luna, Three Arrows Capital, FTX) rather than SEC enforcement alone. However, the regulatory uncertainty made venture funding for crypto startups substantially more difficult and pushed many projects to consider jurisdictions with clearer regulatory frameworks.

2024: The ETF Pivot

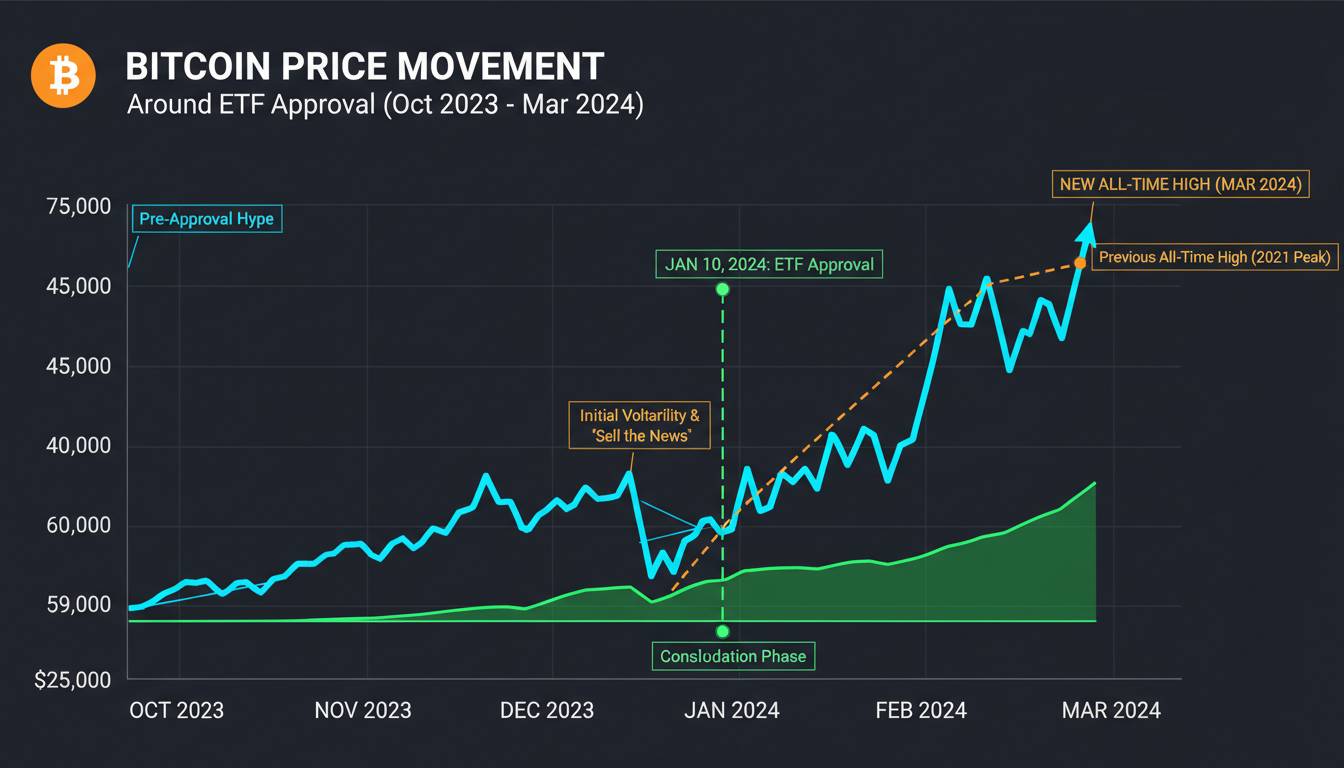

The approval of spot Bitcoin ETFs in January 2024 represents perhaps the most significant single regulatory development in the SEC’s relationship with crypto. After over a decade of rejecting such products, the SEC approved 11 spot Bitcoin ETFs for trading on U.S. exchanges—a decision that immediately transformed how institutional investors could access Bitcoin exposure.

The approvals arrived after Grayscale Investments successfully challenged the SEC’s previous rejection of its Bitcoin ETF application. In August 2023, the D.C. Circuit Court of Appeals ruled that the SEC had acted arbitrarily in approving Bitcoin futures ETFs while rejecting spot Bitcoin ETFs, given the correlation between futures and spot prices. The ruling forced the SEC to reconsider its position, and the agency ultimately approved the products in January.

The market response was immediate and substantial. In the first week of trading, the newly approved ETFs processed over $4 billion in volume. Bitcoin’s price increased approximately 15% in the month following approval, though attributing price movements to a single factor in crypto markets requires substantial caution. More importantly for regulatory dynamics, the approval represented a form of legitimacy that crypto advocates had sought for years—direct SEC oversight of products providing exposure to the largest cryptocurrency.

What the ETF approval did not resolve is the underlying jurisdictional question. The SEC approved these products not because Bitcoin was reclassified as something other than a security, but because specific exchange-traded products met the regulatory standards for listing. The agency maintained its position that Bitcoin itself might be a security while simultaneously approving ETFs that hold Bitcoin. This apparent contradiction reflects the incoherence of applying decades-old securities frameworks to fundamentally novel asset classes.

The Path Forward: Unresolved Tensions

The SEC’s approach to crypto regulation has generated billions of dollars in enforcement penalties and settlements, but it has not produced the regulatory clarity that market participants have repeatedly requested. The fundamental tension remains unresolved: the Howey test was developed in 1946 for orange groves and real estate syndicates, and shoehorning blockchain projects into that framework produces unpredictable and often contradictory outcomes.

Several developments will shape the regulatory landscape in coming years. The outcome of the Ripple case, whenever it finally resolves, will provide important precedent on at least some of the SEC’s theories. Legislative proposals in Congress continue to circulate, though comprehensive crypto legislation has failed to advance despite multiple attempts. The political dynamics around crypto regulation have shifted as well, with some Democratic legislators increasingly open to industry concerns after years of alignment with aggressive enforcement.

What seems clear is that the enforcement-first approach has not achieved its stated goals of protecting investors or bringing clarity to markets. Crypto markets continue to exist, continue to innovate, and continue to generate both legitimate investment opportunities and fraud. The SEC’s choice to prioritize enforcement over rulemaking has left the industry in a perpetual state of uncertainty—notable because regulated markets typically depend on predictability to function effectively.

The spot Bitcoin ETF approval demonstrates that the SEC can facilitate legitimate market access when it chooses to do so. Whether the agency will extend that flexibility to other digital assets, or whether the next enforcement cycle will produce another decade of adversarial confrontation, remains perhaps the central unresolved question in American crypto regulation.