The cryptocurrency regulatory landscape in the United States has shifted significantly, and if you’re holding any digital assets, you need to understand what’s actually happening in Washington. The laws being debated today will shape what you can do with your holdings tomorrow.

Here’s the important distinction that gets lost in viral tweets and sensational headlines: there is no single “crypto bill” that has become law as of early 2025. What exists instead is a fragmented regulatory environment where proposed legislation, administrative actions, and court decisions intersect in ways that directly affect your rights as an investor. The difference between a bill that passed the House and one sitting in committee could determine whether you face new reporting requirements, gain clearer legal protections, or encounter additional restrictions on how you manage your portfolio.

This guide covers the legislative developments that actually matter, explains what they mean for your holdings, and identifies the specific actions you may need to take as the regulatory framework continues to evolve.

The Current State of Crypto Legislation in the United States

The most significant piece of crypto-specific legislation to emerge from Congress in recent years is the Financial Innovation and Technology for the 21st Century Act, commonly known as FIT21. This legislation passed the House of Representatives in May 2024 with a vote of 279-136, representing the most substantial congressional action on digital asset regulation to date. However, FIT21 has not become law. The Senate did not pass the bill before the end of the 118th Congress, which means it would need to be reintroduced and navigate the entire legislative process again.

FIT21’s core purpose was to establish a regulatory framework distinguishing between digital commodities and securities, creating clearer jurisdictional lines between the Commodity Futures Trading Commission (CFTC) and the Securities and Exchange Commission (SEC). The legislation included provisions for consumer protections, defined when a digital asset would be considered a commodity versus a security based on network decentralization, and established registration requirements for crypto exchanges and other platforms. Had it become law, it would have provided the industry with the regulatory clarity it has requested for over half a decade.

The reason FIT21’s fate matters to you is straightforward: without comprehensive federal legislation, regulatory enforcement falls to existing agencies operating under laws written decades before cryptocurrency existed. The SEC, under its previous leadership, pursued numerous enforcement actions against crypto companies, arguing that most digital assets qualified as securities subject to registration requirements. This enforcement-heavy approach created significant uncertainty for holders and platforms alike. The change in SEC leadership in early 2025 has already signaled a shift toward more collaborative regulation, but the fundamental lack of statutory clarity remains unresolved.

Beyond FIT21, several other legislative proposals have circulated in Congress without becoming law. The Clarity for Payment Stablecoins Act addresses stablecoin regulation but has stalled amid disagreements over reserve requirements and issuer licensing. Various amendments to tax reporting requirements have been proposed, some seeking to narrow the scope of current rules and others seeking to expand reporting obligations. The Keep Your Coins Act, introduced by Senator Cynthia Lummis, would allow individuals to hold cryptocurrency in self-hosted wallets without mandatory KYC verification—a proposal that has drawn both praise for protecting financial privacy and criticism for potentially facilitating illicit finance.

Key Regulatory Developments Affecting Your Holdings

While comprehensive legislation remains elusive, several regulatory developments have already altered the operating environment for cryptocurrency holders. The Infrastructure Investment and Jobs Act, signed into law in November 2021, included provisions that significantly expanded crypto tax reporting requirements. Starting in 2024, brokers—including cryptocurrency exchanges—must report transactions to the IRS using Form 1099-DA, providing the agency with detailed information about customer transactions. This represents one of the most consequential regulatory changes for ordinary holders, because it dramatically increases the information the IRS has available to enforce tax compliance.

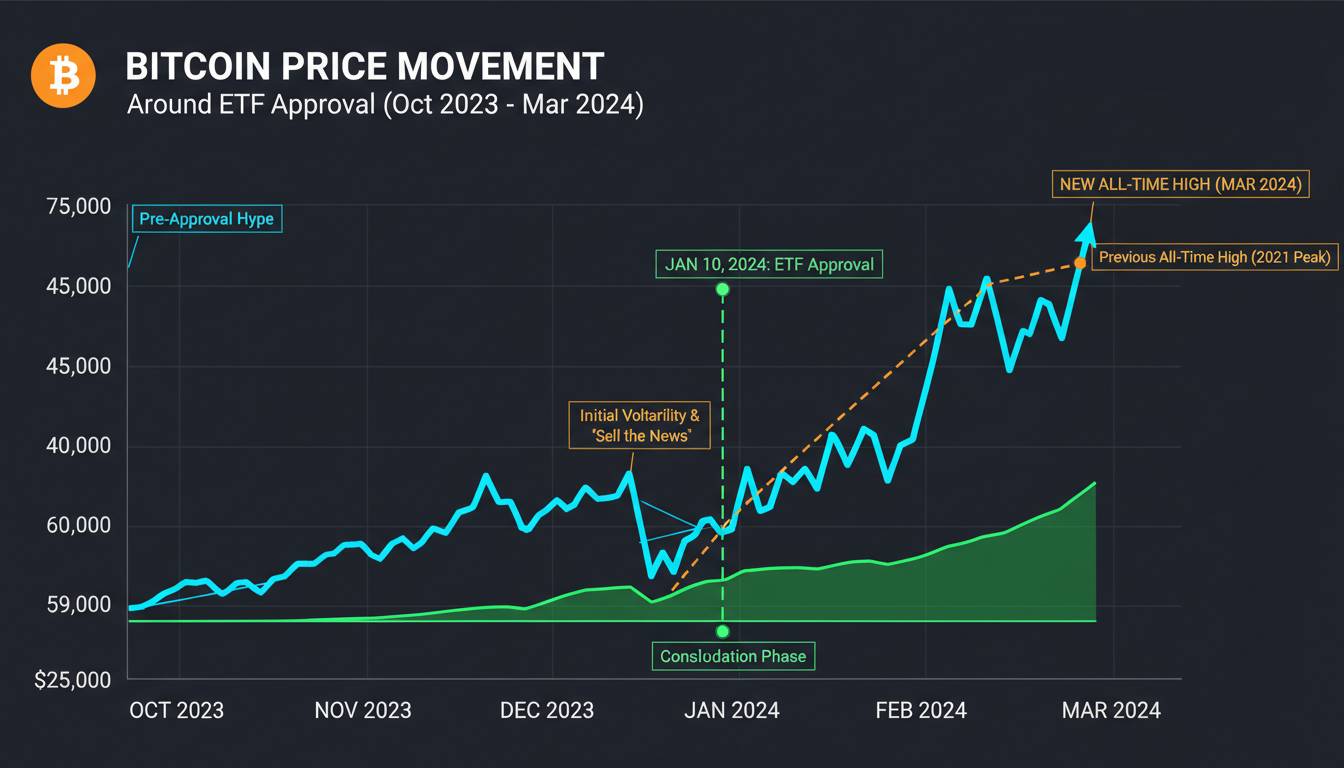

The SEC approved spot Bitcoin exchange-traded funds in January 2024, marking a watershed moment for institutional adoption. While this approval doesn’t constitute new legislation, it represents regulatory acknowledgment that Bitcoin can function within traditional financial markets. The approval process involved years of rejection and legal challenges, with Grayscale Investments successfully suing the SEC in 2023 over the agency’s refusal to approve a Bitcoin ETF. This development has made it easier for retirement accounts and institutional funds to allocate to Bitcoin, potentially affecting both the price dynamics and the regulatory scrutiny applied to the asset class.

The Treasury Department’s Office of Foreign Assets Control (OFAC) has also taken enforcement actions related to cryptocurrency, particularly concerning sanctions violations. In 2022, OFAC sanctioned the Tornado Cash mixer, making it illegal for U.S. persons to use the service—an action that has faced legal challenges on constitutional grounds. For holders, these enforcement actions serve as a reminder that existing sanctions laws apply fully to cryptocurrency transactions, regardless of whether specific crypto legislation exists.

State-level regulation continues to vary significantly, creating a patchwork of requirements that can affect how you hold and trade digital assets. New York’s BitLicense imposes substantial compliance costs on crypto companies operating in the state, costs that are often passed on to customers. Texas and Wyoming have taken more permissive approaches, with Wyoming specifically creating a new bank charter type for crypto companies. This state-level variation means that your experience as a holder may differ substantially depending on where you live and which platforms you use.

What These Changes Mean for Individual Investors

The most immediate impact on your holdings comes from the expanded tax reporting requirements that are already in effect. If you use a centralized exchange for buying, selling, or trading cryptocurrency, that exchange is now required to report your transactions to the IRS. This doesn’t change whether you owe taxes—it changes the likelihood that the IRS will know about your transactions. For holders who have been inconsistent in reporting crypto gains and losses, this represents a significant increase in compliance risk.

The lack of comprehensive legislation creates specific risks that holders should understand. Because no law definitively clarifies which digital assets are securities versus commodities, you may hold assets that could be subject to SEC enforcement action. This isn’t speculation—companies like Ripple, Coinbase, and Binance have faced or are currently facing SEC enforcement actions, and the outcomes of these cases will shape the regulatory landscape regardless of what Congress does. Holding assets that are determined to be securities in violation of registration requirements could theoretically result in forced liquidation or legal liability, though enforcement has typically targeted issuers and platforms rather than individual holders.

For most retail holders, the practical implications are more mundane than alarming. Your ability to buy, sell, and hold cryptocurrency through major exchanges remains largely intact, though the specific assets available may change as platforms adjust their offerings in response to regulatory pressure. Custodial services—where a third party holds your keys—face the most regulatory burden and may impose additional verification requirements or limit certain functionality. Self-custody, where you hold your own keys in a hardware wallet, remains legal and represents the most permissionless option, though it comes with the responsibility of securing your own assets.

Tax Implications and Compliance Requirements

The tax treatment of cryptocurrency hasn’t fundamentally changed with recent regulatory developments—what has changed is the government’s ability to enforce existing rules. The 2021 infrastructure bill’s broker reporting provisions, which fully took effect in 2024, mean that cryptocurrency exchanges must now report customer transactions to the IRS on Form 1099-DA. This applies to transactions involving cryptocurrency, digital assets that can be converted to cash, and certain stablecoins, though the exact scope has been the subject of ongoing regulatory clarification.

For your tax obligations, cryptocurrency remains treated as property in the United States. Buying cryptocurrency with fiat currency is generally not a taxable event, but selling, trading, or using cryptocurrency to make a purchase triggers capital gains or losses. The question of whether mining rewards, staking income, and airdropped tokens constitute taxable income continues to generate confusion, and the IRS has issued guidance indicating that these activities generally result in ordinary income at fair market value when received, with additional capital gains or losses when the received tokens are later sold.

The practical compliance burden has increased substantially. If you have used multiple exchanges, moved assets between wallets, participated in DeFi protocols, or engaged in NFT transactions, you may find that calculating your tax liability requires tracking transactions across numerous platforms and blockchain addresses. The cost basis tracking that exchanges provide through their 1099-DA forms will only cover transactions executed on those specific platforms, meaning that self-custody transfers and non-custodial protocol interactions may need to be tracked manually or with specialized software.

One area where proposed legislation could significantly alter the tax landscape involves wash sale rules. Current tax law prevents taxpayers from claiming losses on the sale of securities if they repurchase substantially identical securities within 30 days. Several proposals have sought to extend this rule to cryptocurrency, which would prevent the common strategy of selling a losing position to realize a tax loss while maintaining exposure through a substantially similar asset. While no such legislation has passed, the possibility remains relevant for holders with significant portfolios.

Timeline and What to Expect Going Forward

Predicting the legislative timeline for crypto regulation in the United States requires acknowledging significant uncertainty. The 2024 elections altered the composition of Congress, and the incoming administration has signaled interest in developing clearer regulatory frameworks for digital assets. However, legislative priorities can shift rapidly, and crypto regulation must compete with numerous other issues on Congress’s agenda.

The SEC’s new leadership under Chair Paul Atkins, appointed in 2025, has indicated a preference for rulemaking through the administrative process rather than exclusively through enforcement actions. This suggests that the agency may develop more specific guidance on which digital assets qualify as securities and what registration requirements apply to different types of crypto businesses. Such guidance, while not legislation, could provide substantial clarity that affects your holdings even without Congressional action.

For FIT21 or similar comprehensive legislation to become law, it would need to navigate both chambers of Congress and secure presidential signature. Given the current political environment, this could happen within the next two years if legislative priorities align, or it could remain stalled indefinitely if disagreements prove insurmountable. The bill’s previous passage in the House provides a template that could be reintroduced and potentially passed more quickly than entirely new legislation, though the Senate’s version would likely differ significantly from the House-passed text.

International developments will also influence the U.S. regulatory landscape. The European Union’s Markets in Crypto-Assets Regulation (MiCA), which began phasing in throughout 2024, provides a comprehensive framework that some U.S. stakeholders view as a model. Whether U.S. legislation adopts similar approaches or maintains distinct domestic frameworks remains to be determined, but the global regulatory environment is increasingly defined by specific rules rather than the absence of them.

Steps You Can Take to Protect Your Holdings

Given the current regulatory uncertainty, several proactive steps can help you protect your holdings and position yourself for whatever regulatory framework eventually emerges.

First, ensure that your tax reporting is accurate and complete. Given the enhanced reporting requirements now in effect, discrepancies between your reported transactions and the information exchanges provide to the IRS are more likely to trigger scrutiny. If you’ve been inconsistent in past reporting, consider consulting a tax professional who specializes in cryptocurrency.

Review where you hold your assets and understand the compliance posture of your platforms. Major exchanges have invested heavily in compliance infrastructure and legal teams, and they are generally positioned to adapt to whatever regulatory framework emerges. Smaller or less established platforms may face greater regulatory risk, and holding significant assets on platforms that cannot survive regulatory scrutiny could result in loss of access to your funds.

Consider whether self-custody makes sense for your situation. Holding your own keys in a hardware wallet provides protection against platform failures and certain regulatory actions targeting custodians, but it also places the full burden of security on you. If you choose self-custody, ensure that you have secure backups of your recovery phrases and understand the risks of loss, theft, or user error.

Document everything. Maintain records of your transactions, cost basis, and any correspondence with tax authorities. In an environment where regulatory requirements are evolving, having thorough documentation provides protection regardless of how the landscape shifts. This includes records of airdropped tokens, staking rewards, and any tokens you may have received through forks or other network events.

Conclusion

The regulatory environment for cryptocurrency in the United States remains fundamentally unsettled, and that uncertainty itself represents a form of risk that holders must manage. No comprehensive crypto legislation has become law, but the enforcement actions of recent years, the tax reporting requirements already in effect, and the various proposals working through Congress mean that the landscape has changed substantially from even two years ago.

What remains constant is that cryptocurrency occupies a meaningful position in the financial ecosystem, and that position will be formalized through either legislation, regulatory guidance, or continued enforcement—likely some combination of all three. The holders who fare best in this environment will be those who maintain accurate records, understand their tax obligations, and recognize that regulatory clarity, when it arrives, will create both new opportunities and new requirements.

Rather than waiting for legislative certainty that may take years to materialize, the pragmatic approach is to ensure your current practices comply with the rules that already exist while remaining adaptable enough to adjust as the framework develops. The most significant risk for most holders is not that cryptocurrency will be banned—it won’t be—but rather that they will face unexpected tax liabilities, compliance penalties, or operational disruptions because they failed to pay attention to developments that were already underway. Stay informed, keep records, and understand that the regulatory landscape will continue to evolve regardless of what Congress ultimately passes.