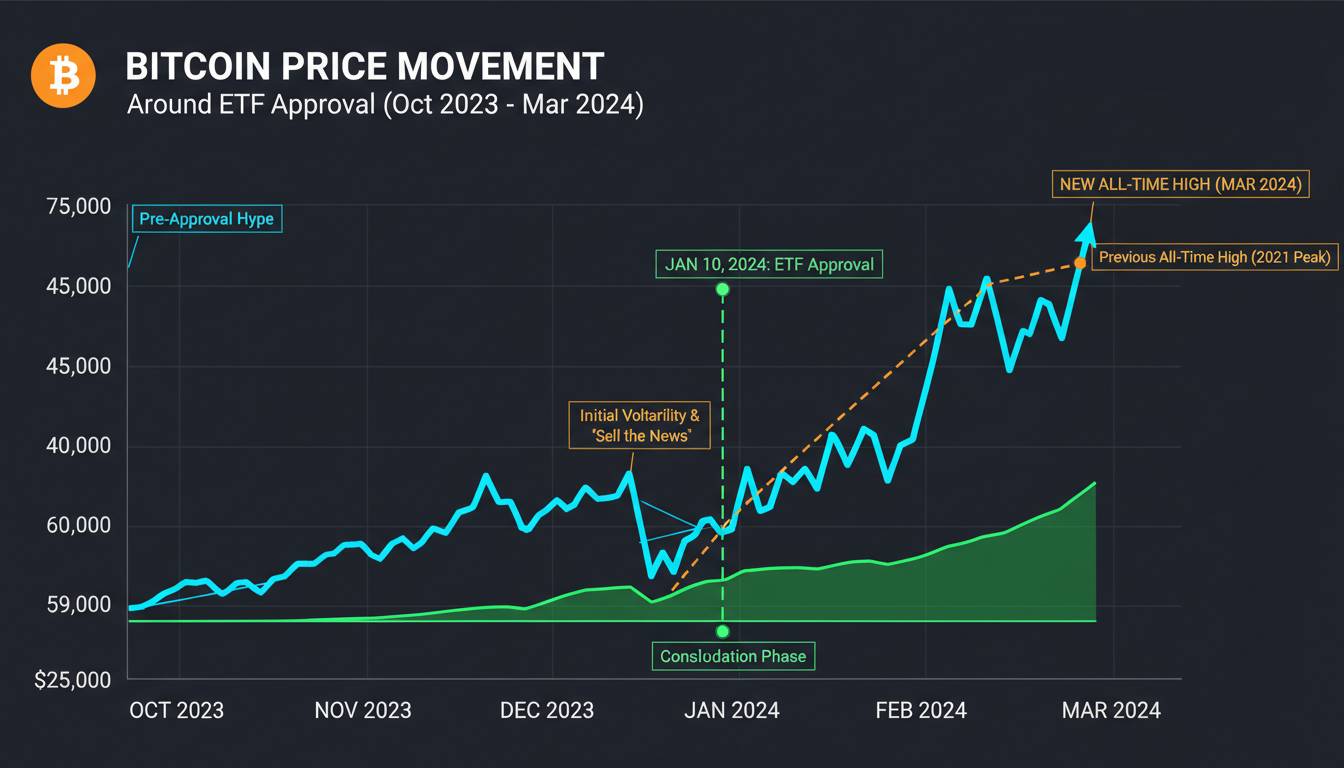

The Securities and Exchange Commission approved spot Bitcoin ETFs in January 2024, a major milestone for cryptocurrency adoption. But Ethereum’s path to ETF approval looks fundamentally different—and understanding why matters for investors watching this space. The distinction touches on staking mechanics, custody complexities, regulatory classification, and what institutional investors actually want from crypto exposure.

Staking: The Make-or-Break Distinction

Bitcoin doesn’t generate yield. Ethereum does. This single fact explains why ETH ETF approval faces hurdles that BTC ETF never encountered.

Staking is how Ethereum network validators earn rewards for securing the blockchain—currently yielding approximately 3-5% annually. When BlackRock, Fidelity, and other asset managers filed their spot Ethereum ETF applications, they initially omitted staking entirely. The SEC made its position clear: including staking would trigger securities law complications because staking rewards could constitute investment contracts.

By mid-2024, issuers amended their filings to exclude staking. Grayscale’s Ethereum Trust trades at significant discounts to NAV because it cannot offer staking yields to shareholders. This creates a structural disadvantage against direct ETH ownership or alternative staking-enabled products. The question now isn’t whether ETH ETFs will launch—the SEC appears increasingly likely to approve them—but whether they’ll launch with staking included. I wouldn’t hold my breath. The regulatory apparatus isn’t equipped to handle yield-generating crypto products at scale, and issuers know this.

If you’re evaluating an ETH ETF against holding Ethereum directly, factor in the approximately 4% annual staking yield you’re sacrificing. For long-term holders, that compounding difference is substantial.

Custody and the “Custody Problem”

Bitcoin custody is straightforward: you hold the private keys, or a custodian does. Ethereum custody involves smart contracts, and that changes everything.

When an ETF holds Ethereum, it must secure not just the tokens but the ability to interact with Ethereum’s decentralized applications, staking validators, and increasingly complex DeFi infrastructure. The custody landscape for ETH is fragmented in ways BTC custody never was. Third-party custodians like Coinbase Custody, BitGo, and Fidelity Digital Assets have built robust BTC custody solutions. ETH custody requires additional technical infrastructure—securing validator keys, managing slashing risk, and navigating the evolving validator landscape.

The collapse of several ETH staking providers in 2022-2023 highlighted custody vulnerabilities that BTC custodians never faced. Bitcoin can be held in cold storage with minimal technical complexity. Ethereum’s interoperation with smart contracts creates attack surfaces that make institutional custodians cautious.

Until custody solutions mature significantly, expect higher expense ratios on ETH ETFs compared to BTC ETFs. You’re paying for the additional operational complexity.

Regulatory Classification: The Ongoing Debate

The SEC has historically treated Bitcoin and Ethereum differently, and that distinction hasn’t disappeared—it has merely been temporarily set aside during the BTC ETF approval process.

SEC Chair Gary Gensler repeatedly emphasized that Bitcoin was a commodity during the approval hearings, suggesting ETH might face different treatment. While the SEC approved ETH futures products in 2023, spot ETH ETFs present a different regulatory question. The CFTC asserts oversight over Bitcoin as a commodity, but Ethereum’s classification remains legally ambiguous.

Ethereum’s transition to proof-of-stake in September 2022 added fuel to this debate. Staking involves network participants effectively delegating their coins to validators—a structure that resembles investment contracts to some legal analysts. The SEC’s Howey test doesn’t cleanly accommodate decentralized network tokens.

Regulatory uncertainty is priced into ETH ETF expectations. Expect volatility around approval announcements that exceeds what we saw with Bitcoin ETFs.

Market Structure and Liquidity Differences

Bitcoin’s market is larger and more liquid than Ethereum’s, but the gap is narrower than most assume—and it’s closing.

As of early 2025, Bitcoin’s market capitalization sits around $800 billion, while Ethereum approaches $250 billion. Daily trading volumes for BTC exceed ETH by roughly 3:1. However, ETH’s derivatives market is disproportionately large compared to its spot market—a factor that could influence how ETF authorized participants create and redeem shares.

Spot ETF creation requires significant capital efficiency. When market makers create ETF shares, they must acquire underlying assets. ETH’s more concentrated holder base and larger institutional positions could create tighter spreads initially but potentially more volatile creation/redemption dynamics. The Grayscale Ethereum Trust has traded at steeper discounts than its Bitcoin counterpart, reflecting these structural concerns.

ETH ETFs may experience wider bid-ask spreads and more pronounced premium/discount dynamics than BTC ETFs, especially in early trading.

Tax Implications: The Wash Sale Rule Loophole

Here’s something most coverage overlooks: ETH ETFs might actually offer tax advantages that BTC ETFs don’t.

Bitcoin ETF holders face the same wash sale rule constraints as direct Bitcoin ownership. If you sell at a loss and repurchase within 30 days, you cannot claim the loss. However, some structured products based on Ethereum have been classified differently by the IRS, creating potential tax efficiency opportunities that pure spot exposure doesn’t offer.

This remains an evolving area. The IRS has not issued definitive guidance on spot crypto ETF taxation, and the distinction between commodity-based ETFs and synthetic products could matter significantly. Early indications suggest ETH-based products may navigate this landscape differently, but expect continued ambiguity.

Consult a tax professional before treating ETH and BTC ETFs identically from a tax planning perspective. The regulatory gray areas are substantial.

The Approval Timeline: What History Suggests

Bitcoin’s ETF journey took over a decade from first application to approval. Ethereum’s path might be shorter—or it might not.

Cumberland’s Chris Terry noted that Ethereum could see approval within weeks of a favorable SEC decision, compared to Bitcoin’s multi-year odyssey. The regulatory framework, while not settled, has precedent from the BTC approval. However, the staking question adds complexity that Bitcoin never presented.

The SEC delayed multiple ETH ETF decisions throughout 2024, pushing potential approval into 2025. Unlike Bitcoin, where the SEC’s resistance eventually crumbled under political and legal pressure, Ethereum’s case hasn’t reached that inflection point. The approvals might come suddenly—these regulatory decisions often do—or they might require another cycle of applications and rejections.

Position your investment thesis around the possibility of approval rather than a specific timeline. The volatility around announcement dates will likely exceed post-approval trading ranges.

Institutional Adoption: Different Players, Different Appetites

The institutional players interested in Ethereum differ from those who adopted Bitcoin ETFs—and their appetite might be smaller.

BlackRock’s Larry Fink has been notably more cautious about Ethereum than Bitcoin, describing BTC as “an international asset” while positioning Ethereum more as a technology play. The largest institutional adopters of BTC ETFs—hedge funds, family offices, retirement platforms—may find ETH’s yield story compelling, but many have internal policies restricting allocation to assets below certain market capitalization thresholds.

Ethereum’s more complex technical architecture also makes it harder for traditional institutions to evaluate. Understanding staking slashing risk, validator economics, and smart contract exposure requires more sophistication than holding Bitcoin. This isn’t a criticism—it’s a reality that will limit initial adoption.

Expect more measured institutional allocation to ETH ETFs compared to the immediate billions flowing into BTC ETFs. The learning curve is steeper.

The Verification Problem: What We Don’t Know

I need to be honest: several critical questions about ETH ETF approval remain genuinely unanswered, and anyone claiming certainty is guessing.

We don’t know whether the SEC will require ETH ETFs to disable staking functionality entirely or whether some limited staking permission might be approved. We don’t know how the incoming SEC leadership under a new administration will approach Ethereum classification. We don’t know whether Ethereum’s institutional custody infrastructure will be ready when approvals come, or whether delays will stem from operational limitations rather than regulatory ones.

The Bitcoin ETF approval became clearer over time because Bitcoin’s regulatory status was more settled. Ethereum remains genuinely uncertain on multiple dimensions simultaneously. That’s not a reason to avoid the topic—but it is a reason to hold your convictions loosely.

Build flexibility into your ETH ETF thesis. The product will likely launch, but the exact structure and timing remain genuinely uncertain.