The SEC’s approval of Bitcoin ETFs on January 10, 2024 ended a decade-long regulatory battle over cryptocurrency investment products. But the path Ethereum ETFs will take—and in some cases, have already begun to take—looks meaningfully different. Understanding why requires retracing the Bitcoin ETF approval timeline, examining the asset class distinctions that complicate Ethereum’s regulatory treatment, and recognizing how the SEC’s posture has shifted since that January decision.

The Bitcoin ETF Approval Timeline: A Decade in the Making

Bitcoin ETF proposals didn’t begin in 2023. The first serious application arrived in 2013, when the Winklevoss twins filed their proposal with the SEC. That application, and nearly every one that followed for the next decade, faced rejection. The SEC consistently cited concerns about market manipulation, the lack of regulated surveillance-sharing agreements between crypto exchanges and traditional financial markets, and questions about whether Bitcoin markets were sufficiently transparent and trustworthy to support an ETF.

The turning point came from legal pressure, not regulatory epiphany. Grayscale Investments, which operated the Grayscale Bitcoin Trust (GBTC), sued the SEC after the commission rejected its ETF application in 2022. The company’s argument was straightforward: the SEC had already approved Bitcoin futures ETFs in 2021, which meant the commission had determined Bitcoin markets were sufficiently regulated. Denying spot Bitcoin ETFs while allowing futures ETFs was arbitrary and capricious.

In August 2023, the D.C. Circuit Court of Appeals agreed. It ruled that the SEC had failed to adequately explain why it approved Bitcoin futures ETFs but rejected spot Bitcoin ETFs. The court vacated the SEC’s rejection order and sent the matter back for reconsideration.

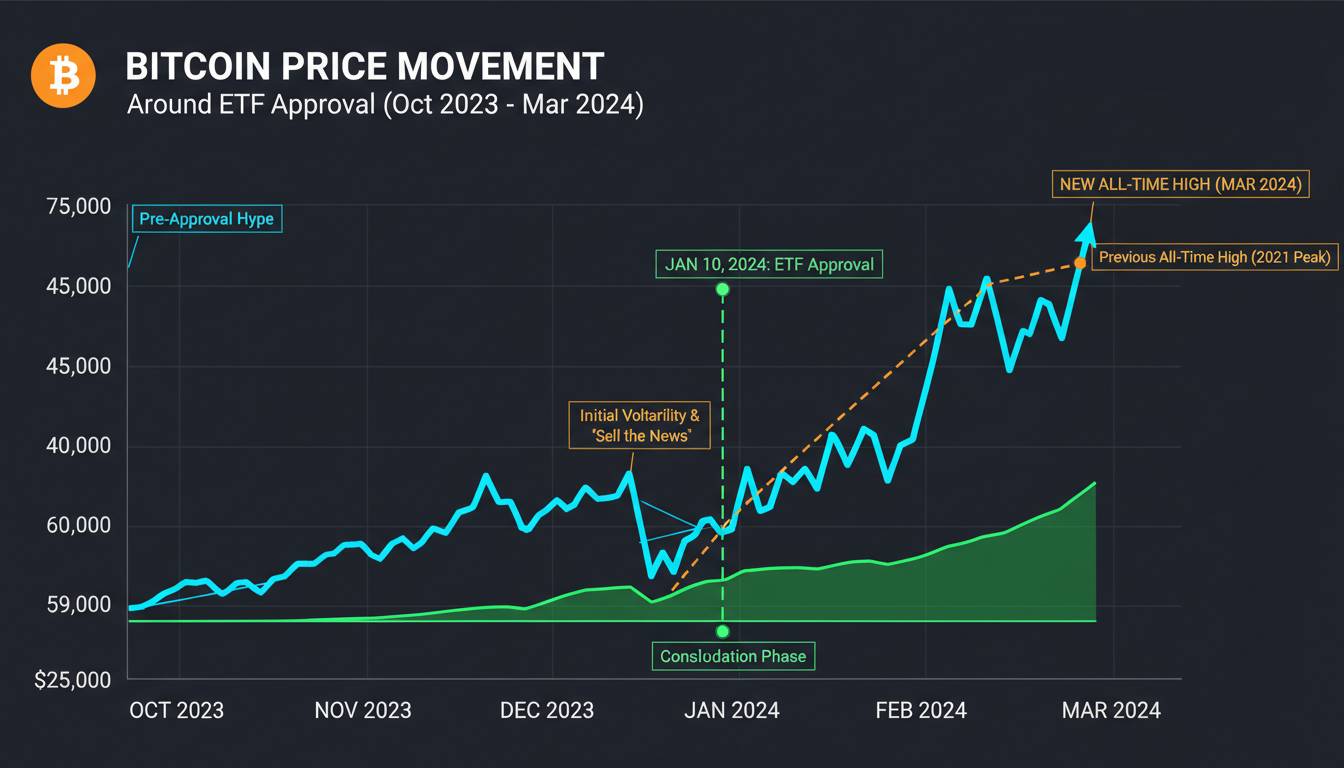

This legal loss created enormous pressure on the SEC. Rather than continue fighting through what would likely be years of additional litigation, the commission essentially blinked. Between October 2023 and January 2024, the SEC engaged in rapid discussions with major financial institutions including BlackRock, Fidelity, Invesco, and others who had filed fresh applications. On January 10, 2024, the SEC approved 11 spot Bitcoin ETFs in a single day, marking the most significant development in crypto regulation since the 2017 ETF rejections.

The entire process—from the first application to final approval—spanned roughly eleven years. The Ethereum ETF timeline will almost certainly be shorter, but not because the regulatory questions are easier.

How Ethereum Differs From Bitcoin as an ETF Asset

The most important distinction between Bitcoin and Ethereum for ETF purposes isn’t technological—it’s regulatory. Bitcoin has been classified as a commodity by the CFTC since 2015, and that classification has never been seriously contested in the context of ETF approval. SEC Chair Gary Gensler repeatedly confirmed during Congressional testimony that Bitcoin is a commodity, not a security. This clarity eliminated one major obstacle that Ethereum still faces.

Ethereum’s classification is genuinely contested. The SEC’s 2023 lawsuit against Coinbase and Binance alleged that multiple cryptocurrencies, including Ethereum, qualified as securities under the Howey test. While the CFTC has long argued Ethereum is a commodity (and currently regulates Bitcoin and Ethereum as commodities in futures markets), the SEC’s enforcement actions created regulatory ambiguity that doesn’t exist for Bitcoin.

This matters enormously for ETFs because the SEC’s resistance to spot crypto ETFs has historically centered on concerns about securities law compliance and investor protection. A spot Bitcoin ETF holds a commodity; a spot Ethereum ETF might hold a security, depending on how the SEC ultimately rules on Ethereum’s classification.

Beyond the classification question, Ethereum introduces a second complication that Bitcoin doesn’t have: staking. Ethereum transitioned to proof-of-stake in September 2022, meaning ETH holders can “stake” their tokens to help secure the network and earn yield. This creates a yield-bearing asset where Bitcoin is purely a store of value. The SEC has historically been skeptical of any financial product that generates returns through network participation, viewing staking programs as potential securities offerings. Several issuers have already filed Ethereum ETF applications that explicitly exclude staking—the ETF will hold plain ETH without attempting to generate staking rewards. Whether this concession satisfies the SEC remains to be seen.

Custody arrangements also differ. Bitcoin’s custody for ETFs is relatively straightforward: the ETF holds private keys in cold storage at a regulated custodian. Ethereum requires more complex custody because the Ethereum network supports smart contracts and multiple token standards. A custodian must be capable of securing not just ETH but also any ERC-20 tokens that might be associated with the holdings. Most traditional custody providers have built out Ethereum capabilities, but the operational complexity exceeds what Bitcoin requires.

The Ethereum ETF Approval Process: What Has Happened So Far

As of early 2025, Ethereum ETFs have already completed a significant portion of their regulatory journey. The SEC approved several Ethereum ETF applications in 2024, following a process that moved faster than most analysts expected given the regulatory uncertainty surrounding Ethereum’s classification.

The initial wave of Ethereum ETF applications arrived in late 2023 and early 2024, mirroring the Bitcoin ETF filing rush. BlackRock, Fidelity, Invesco, Grayscale, and others submitted 19b-4 forms to the SEC. The commission initially delayed decisions repeatedly, extending the review period as it had done with Bitcoin ETF applications for years. Market participants widely expected the SEC to reject these applications, pointing to the classification uncertainty and the agency’s historical hostility toward crypto ETFs.

However, the political and legal environment shifted. The D.C. Circuit’s Grayscale ruling applied pressure not just to Bitcoin but to any crypto ETF review. More importantly, the SEC’s posture changed following the Bitcoin ETF approvals—the commission had essentially conceded that spot crypto ETFs were permissible products if issuers could meet certain surveillance-sharing and custody standards. Several Ethereum ETF applicants restructured their proposals to exclude staking, addressing one of the SEC’s primary concerns about securities classification.

The approvals came in May 2024, when the SEC greenlit multiple Ethereum ETF applications. Trading began shortly after, making Ethereum the second cryptocurrency to have a regulated spot ETF trading on U.S. exchanges.

This timeline—from application to approval—compressed into approximately six months for Ethereum, compared to the decade-long odyssey for Bitcoin. The accelerated process reflects lessons learned from the Bitcoin ETF review and the commission’s recognition that rejecting Ethereum ETFs while approving Bitcoin ETFs would be difficult to defend legally.

Why the SEC Approved Bitcoin ETFs Before Ethereum

The SEC approved Bitcoin ETFs first for reasons that combine legal precedent, asset classification clarity, and institutional momentum.

The Grayscale lawsuit created binding legal pressure that didn’t exist for Ethereum. When the D.C. Circuit ruled that the SEC’s rejection of spot Bitcoin ETFs was arbitrary given its approval of Bitcoin futures ETFs, the commission had a clear legal vulnerability. No equivalent lawsuit had forced the SEC to reconsider Ethereum ETF applications before 2024. Ethereum futures ETFs exist, but the legal argument connecting futures and spot approval is weaker than it was for Bitcoin because Ethereum’s futures market is smaller and the SEC’s earlier Ethereum-related enforcement actions created more complicated precedent.

Asset classification played an equally important role. The SEC’s resistance to crypto ETFs always centered on investor protection concerns tied to securities law. By approving Bitcoin ETFs, the commission implicitly accepted that a commodity-based spot ETF could proceed under existing regulations if certain conditions were met. Ethereum’s potential securities classification created additional legal questions that the commission didn’t need to answer for Bitcoin. The May 2024 approvals suggest the SEC ultimately concluded Ethereum ETFs could proceed under a similar framework, likely treating Ethereum as functionally equivalent to Bitcoin for ETF purposes despite the ongoing classification debate in broader enforcement contexts.

Market maturity mattered too. Bitcoin’s spot market is larger, more liquid, and more heavily surveilled than Ethereum’s. While both markets have significant trading volume, Bitcoin’s dominance and simpler technological structure made it the logical first candidate for ETF approval. The SEC could point to specific surveillance-sharing arrangements with Bitcoin exchanges that satisfied its market integrity concerns. Replicating those arrangements for Ethereum took additional time and coordination.

What Made Bitcoin ETF Approval Possible After Years of Rejection

The Bitcoin ETF approvals in January 2024 weren’t simply the SEC changing its mind—they resulted from specific developments that addressed the commission’s stated concerns.

First, the Grayscale ruling eliminated the SEC’s legal authority to continue rejecting applications on procedural grounds. The court made clear that the SEC couldn’t approve futures ETFs while rejecting structurally similar spot ETFs without offering a coherent explanation. This forced the commission to the negotiating table rather than simply issuing another rejection order.

Second, surveillance-sharing agreements between crypto exchanges and Nasdaq and NYSE satisfied the SEC’s demand for market integrity protections. These agreements allow the exchanges to access trading data from major Bitcoin trading venues, enabling detection of market manipulation. The SEC had insisted on such arrangements for years; their completion in 2023 removed a primary objection.

Third, institutional participation had reached a critical mass that made continued rejection untenable. BlackRock, the world’s largest asset manager with $10 trillion in assets under management, filed its Bitcoin ETF application in 2023. The SEC had repeatedly indicated it would prefer to regulate crypto through registered products offered by established financial institutions rather than driving institutional investors into unregulated structures. BlackRock’s involvement effectively made Bitcoin ETF approval a matter of when, not if.

Fourth, the political environment shifted. By late 2023, multiple members of Congress had publicly urged the SEC to approve Bitcoin ETFs. Several federal judges had ruled against the SEC in crypto-related cases. The commission’s hardline stance had become legally and politically unsustainable.

Ethereum benefited from each of these developments. The legal precedent set by Grayscale applied to Ethereum as much as Bitcoin. Surveillance-sharing infrastructure built for Bitcoin could extend to Ethereum. BlackRock and Fidelity filed Ethereum ETF applications alongside their Bitcoin products. The SEC found itself in a position where rejecting Ethereum ETFs would require explaining why the asset class that generated the second-largest spot market and supported the largest DeFi ecosystem couldn’t meet the same standards as Bitcoin.

Key Differences in the Regulatory Treatment of Bitcoin vs Ethereum ETFs

Despite the similarities in how the SEC ultimately approached both products, several meaningful differences distinguish the Bitcoin and Ethereum ETF approval processes.

The timeline compression stands out immediately. Bitcoin ETFs took eleven years from first application to approval. Ethereum ETFs moved from initial filing to approval in approximately six months. This acceleration reflects both the legal precedent set by Bitcoin’s approval and the SEC’s apparent decision that maintaining separate regulatory timelines for Bitcoin and Ethereum would invite additional litigation.

Staking became a central question for Ethereum that has no Bitcoin equivalent. The SEC’s concerns about staking programs as potential securities offerings forced Ethereum ETF issuers to make a choice: include staking and risk rejection, or exclude staking and offer a product that doesn’t capture one of ETH’s distinctive features. Most applicants chose the latter, filing amendments that explicitly prohibited staking. This means the approved Ethereum ETFs hold ETH essentially the same way Bitcoin ETFs hold BTC—as a passive holding without yield generation. Whether this limitation makes the products less attractive to investors who might otherwise hold ETH directly remains an open question.

The classification debate continues to shadow Ethereum in ways it doesn’t shadow Bitcoin. The SEC’s approval of Ethereum ETFs doesn’t constitute a formal ruling that Ethereum is a commodity rather than a security. It’s best understood as a regulatory accommodation that allows institutional investors exposure to ETH through a regulated product without the SEC formally resolving the underlying classification question. This ambiguity doesn’t exist for Bitcoin—everyone agrees Bitcoin is a commodity. Ethereum’s status remains contested, and future enforcement actions could theoretically create complications for the ETF structure, though the SEC would likely face significant legal challenges if it attempted to unwind an approved ETF based on securities classification.

Custody requirements are more complex for Ethereum, as noted earlier. This didn’t prevent approval, but it added operational considerations that ETF issuers and their custodians needed to address. The approved Ethereum ETFs have all met these requirements, but the additional complexity created more points of potential failure during the approval process.

What Investors Should Know About These Differences

If you’re considering an Ethereum ETF, understanding these distinctions matters for several practical reasons.

The staking exclusion means Ethereum ETFs will underperform direct ETH holdings in any period where staking yields are positive. Staking rewards on Ethereum currently range from 3% to 5% annually, depending on network conditions. An investor choosing an ETF over direct ownership is accepting this yield sacrifice in exchange for institutional custody, regulatory clarity, and the ability to hold the position in a traditional brokerage account alongside other retirement or taxable investments. For many investors, particularly those holding crypto in tax-advantaged accounts or through custodians who don’t support staking, the ETF structure makes sense regardless of the yield difference.

The classification ambiguity means Ethereum ETF approval doesn’t resolve the broader regulatory uncertainty surrounding Ethereum. The SEC could theoretically pursue enforcement actions against Ethereum’s underlying structure while allowing ETFs to continue trading. This seems unlikely given the legal gymnastics it would require, but the distinction matters for investors who want maximum regulatory certainty.

The compressed timeline for Ethereum ETFs reflects both regulatory learning and legal pressure that may not persist. If the SEC faces a different legal outcome in a future case, or if political winds shift, the path for additional crypto ETFs could become more complicated. The ease with which Ethereum ETFs received approval shouldn’t be assumed to apply universally to other cryptocurrencies.

Conclusion: What Remains Unresolved

The approval of both Bitcoin and Ethereum ETFs represents a fundamental shift in how institutional investors can access cryptocurrency markets. What started as a decade-long rejection of Bitcoin ETFs has, in roughly eighteen months, produced approved products for the two largest cryptocurrencies by market capitalization.

But significant questions remain. Will the SEC eventually clarify Ethereum’s regulatory classification, or will the ETF approval serve as a de facto classification that avoids the formal determination? How will the exclusion of staking from Ethereum ETFs evolve—might some issuers eventually seek approval for staking-enabled products if the regulatory environment becomes more accommodating? And perhaps most importantly, what does this mean for investors hoping to access other cryptocurrencies through regulated ETF products? The answers will depend on litigation outcomes, political developments, and the SEC’s willingness to treat cryptocurrency markets with the same regulatory framework applied to other commodities.

For now, the Bitcoin and Ethereum ETF approvals have established a template. Whether that template expands to cover additional assets or contracts based on future regulatory decisions remains the most important unresolved question in this space.